A citizen-led ballot initiative to amend the WA Cares Act would allow workers to opt out of a state long-term care insurance program, but would likely effectively kill it, too. The 2019 legislation created a public long-term care insurance program that provides older, injured or disabled people up to $36,500 to pay for long-term care services and needs, like nursing home care, equipment, medication and meals. To pay for the program and access the benefits, workers are required to pay a 0.58% tax, which started in July 2023.

Initiative 2124 would amend the act, adding the ability for anyone to opt out of the program at any time. Anyone who opts out would not be paying into the program and would therefore not be able to access the benefits should they need them later in life.

This is how the proposition is worded on your ballot:

Initiative Measure No. 2124 concerns state long term care insurance.

This measure would provide that employees and self-employed people must elect to keep coverage under RCW 50B.04 and could opt-out any time. It would also repeal a law governing an exemption for employees. This measure would decrease funding for Washington’s public insurance program providing long-term care benefits and services.

Should this measure be enacted into law?

Yes

No

The initiative was fronted by Let’s Go Washington, a multimillionaire-backed group that also brought citizens’ initiatives to this year’s ballot aimed at repealing programs and policies meant to slow climate change, and another aimed at repealing the state’s wealth tax.

What is the program?

WA Cares became law in 2019 as one of the first of its kind in the nation and is slated to start paying out in July 2026. Originally called the The Long-Term Services and Supports Trust Act, it started with the recognition that people are aging and most will need long-term care at some point.

Right now, most workers in the state are required to participate in the program and pay the tax. That is, unless they are a federal employee, if they live out of state but work in Washington, secured their own long-term care insurance coverage and opted out during a six-month window before December 2022, or fall under other exemptions

The 0.58% tax (though it’s technically a premium) amounts to 58 cents per $100. For the median-income earner in Spokane County making $73,583 annually, they pay about $35 per month. Washington doesn’t have a state income tax, so the only other state taxes coming out of paychecks are for state Family and Medical Leave Insurance and state Workers’ Comp.

Let’s Go Washington, the group behind the initiative against WA Cares, argues that too many workers have to pay into the fund who may never use it or qualify for it. In order to qualify, participants must have contributed for a minimum number of years before applying, which is either at least 10 years without a gap of five or more consecutive years, or for three of the last six years before applying. The program has also opened up partial eligibility to recent retirees.

Washingtonians can also see approximately how much they will contribute to the fund over their lifetime by entering their current age and income into the program website.

WA Cares covers program participants who have a care need, defined as “if you need assistance with three or more activities of daily living, such as bathing or managing medications.” While this would mainly include elderly people, it also includes people who become disabled and can no longer care for themselves, like if you got a traumatic brain injury in a car crash. Uses for the funds include paying for a part-time caretaker; off-setting costs of equipment, like a wheelchair or a wheelchair ramp; medication; getting assistance with bathing; and room and board in an adult-care facility for a few months.

However, the program has a lifetime payout cap of $36,500 (though it would adjust for inflation), which is one of the biggest criticisms against it, as long-term care costs can easily exceed that.

Nursing homes broadly average $4,500 per month nationally, according to the National Council on Aging. Private long-term care insurance can also be cost-prohibitive and the market volatile. Medicaid, which is a federal program, doesn’t cover long-term care unless a person meets strict income limits and first spends down their savings and assets. Medicare, another federal health care program, doesn’t cover long-term care at all.

The program is intended to be of modest assistance in helping offset costs for elderly or disabled Washingtonians to be able to stay in their homes and still get care. Program Director Ben Veghte told the WA State Standard last year that the program is a first step and thinks the state needs to enhance and build on it.

In 2019, 62.9% of voters wanted to repeal the act, though it was a non-binding advisory vote, which is essentially a poll. In 2020, 54.36% of voters rejected a constitutional amendment that would have allowed for the fund to be invested in the stock market, in an effort to help it grow much faster. Post-election polling of that ballot item pointed to voters not understanding what it was and feeling uneasy about the stock market during the pandemic. The pandemic then pushed back the implementation of the program by several years.

One big criticism against the program early on was that people wouldn’t be able to take the benefit with them should they move out of state later in life. The state addressed that in 2022 and made benefits available for out-of-state participants starting in July 2030.

What the initiative would do if passed

Initiative 2124 would give anyone the ability to opt out of the program and require that people elect to keep their coverage. Let’s Go Washington has billed it as “giving workers a choice.”

If passed, workers who opt out would stop paying the tax but be unable to access the benefit should they need it later. They also would not get back any money they’ve paid into the program.

WA Cares is still in its infancy, which is one of the reasons why Initiative 2124 would deal a likely fatal blow to it: Much like a regular insurance policy, the program needs a lot of people paying in to keep the costs low for everyone, according to a 2022 Actuarial Study for the state.

The same study determined that the program was solvent and would stay solvent for the next 75 years, based on projections and estimated future revenue through a mandatory program.

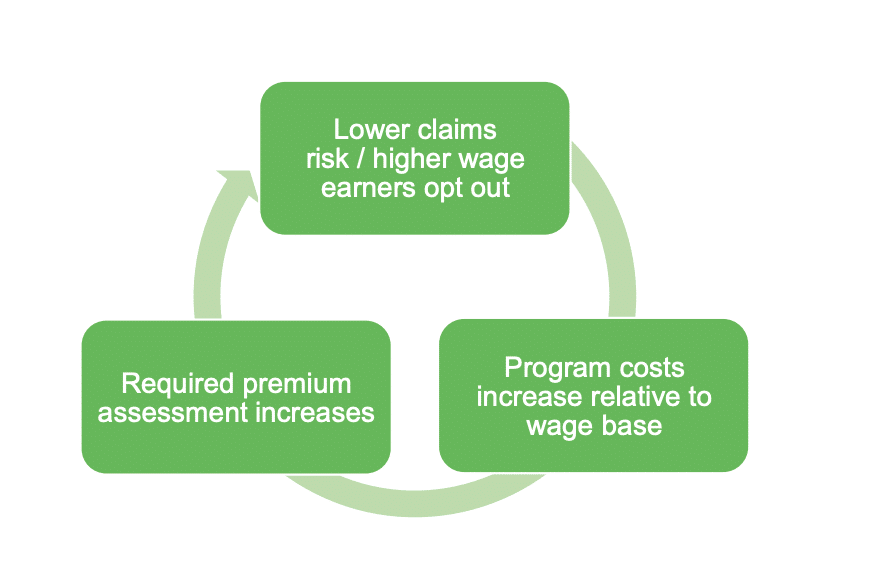

A 2023 study by the same actuary firm modeled what would happen if the program was fully voluntary — as the initiative proposes — and described an “insurance rate spiral,” in which people who either make higher wages or are less likely to need the care opt out, causing program costs and premiums to rise, leading more people to opt out and so on.

Opponents of the initiative say it will effectively repeal the program by triggering exactly this kind of financial death spiral. Even more, it would cost the state — and ultimately the program itself — between $12.6 million and $31.2 million just to deal with people opting out, according to the fiscal impact statement in the voters’ guide.

Further reading

To find more information and opinions from Let’s Go Washington, the group pushing for “yes” votes on the initiative, click here.

To find more information and opinions from Defend WA, one of several groups pushing for “no” votes on the initiative to protect the state’s long-term care program, click here.

To read more about the program itself, click here.

For even further reading on the initiative, check out the news articles below.

- Initiative 2124 will ask voters if they want to make long-term care insurance optional, which could doom the WA Cares Fund - Eliza Billingham, The Inlander

- Initiative 2124 would make WA Cares insurance program tax optional - John Stang, Cascade PBS

- Making WA’s long-term care program optional will create costs for state - Jerry Cornfield, WA State Standard

- Why supporters of Washington’s long-term care program worry about Initiative 2124 - Laurel Demkovich, WA State Standard via Cascadia Daily News